Mathematical Modelling

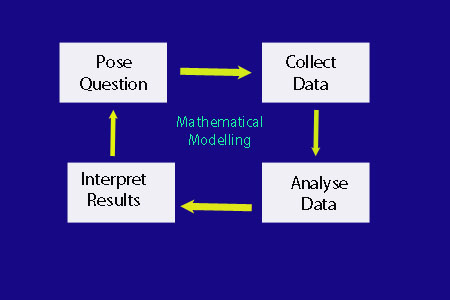

Mathematical modelling helps solve real‑world problems by finding relationships between variables that describe the situation being examined.

Once a question is posed, data is collected, analysed and interpreted to look for patterns or relationships that can be used to test the model and make predictions.

This is often an iterative process — the model is tweaked and repeated until an acceptable outcome is reached.

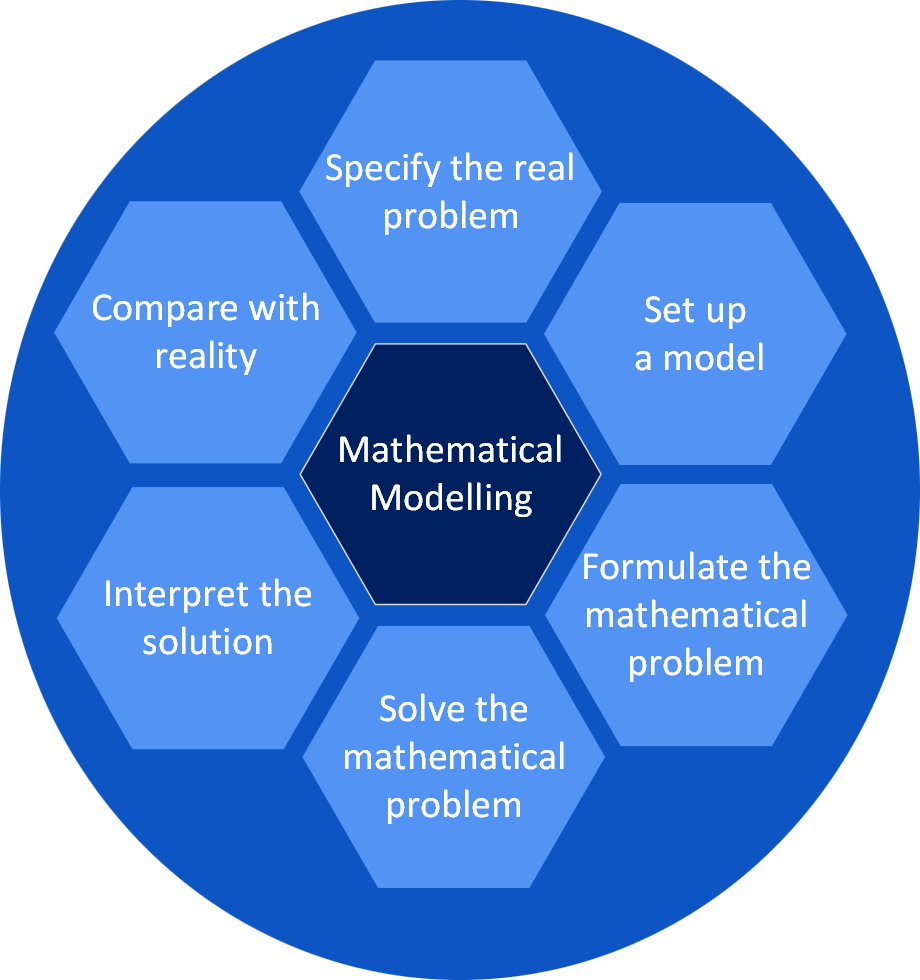

Modelling Stages

1. Specify the real problem

- What exactly is the problem the model needs to address?

- Simplify the problem and identify its most important features.

2. Set up a model

- Specify assumptions

- Choose appropriate variables

- Specify relationships

- Specify parameters

- Specify data to be collected

3. Formulate the mathematical problem

- Identify the dependent variable

- Write down relevant potential formulae

- Sketches can be helpful

- Recurrence relationship?

- Differential equation?

- Optimisation problem?

4. Solve the mathematical problem

- Use relevant mathematical skills

5. Interpret the solution

- What do the results mean?

- Do graphs show any relationships?

- Have any useful equations been formulated?

6. Compare with reality

- Test the model with real data

- Is it realistic?

- What improvements can be made?

A person wishes to buy a car using an unsecured bank loan.

- £550 is available for monthly repayments.

- The loan can last 3, 4 or 5 years.

Question: What is the top of the car price range that is affordable?

1. Specify the real problem

How much can be borrowed if the monthly repayment is £550?

The amount borrowed depends on the interest rate and the loan term.

2. Set up a model

Interest rates vary between lenders, so several representative rates will be considered for 3, 4 and 5‑year terms.

| Lender | Annual Rate |

|---|---|

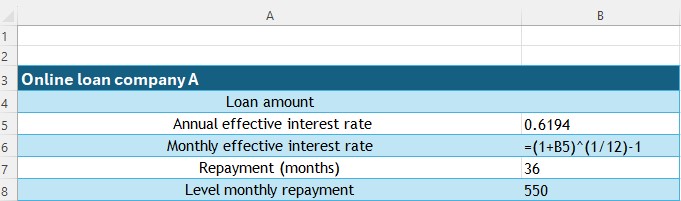

| Online loan company A | 61.94% representative |

| Online loan company B | 19.9% representative |

| Own Bank | 6.2% |

Assume the representative rate is fixed for the duration of the loan.

Variables: interest rate and number of repayments.

Number of monthly repayments: 36, 48 or 60.

Total monthly repayment must not exceed £550.

First go around

3. Formulate the mathematical problem

As a first approximation, assume the monthly payments are saved in an account.

The balance after each term would be:

- 36 × £550 = £19,800

- 48 × £550 = £26,400

- 60 × £550 = £33,000

The account balance equals the interest paid plus the original capital borrowed.

4. Solve the mathematical problem

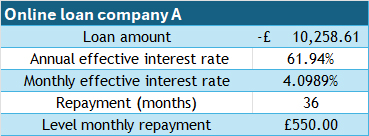

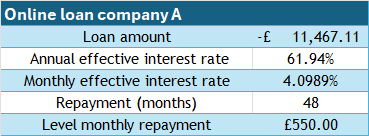

Online loan company A — 61.94% interest

3 years:

£4,662.33

4 years:

£3,838.73

5 years:

£2,963.08

Online loan company B — 19.9% interest

3 years:

£11,487.03

4 years:

£12,774.01

5 years:

£13,317.36

Own Bank — 6.2% interest

3 years:

£16,530.72

4 years:

£20,754.19

5 years:

£24,428.19

5. Interpret the solution

A monthly repayment of £550 would service a loan from just under £3,000 to just under £25,000.

6. Compare with reality

The results seem very low. This basic model assumed interest was compounded yearly and did not take repayments into account.

Second go around

2. Set up a model

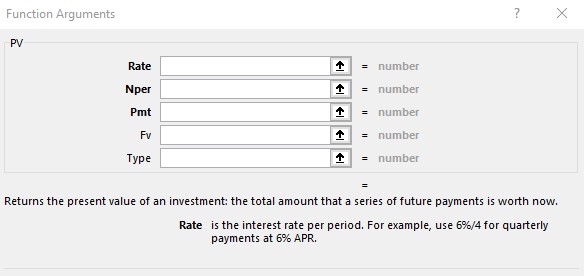

Create an Excel spreadsheet using the PV function to calculate the present value of a loan or investment based on a constant monthly interest rate.

This requires the following variables:

- Rate — the monthly effective interest rate.

- Nper — total number of payment periods.

- Pmt — fixed monthly repayment.

3. Formulate the mathematical problem

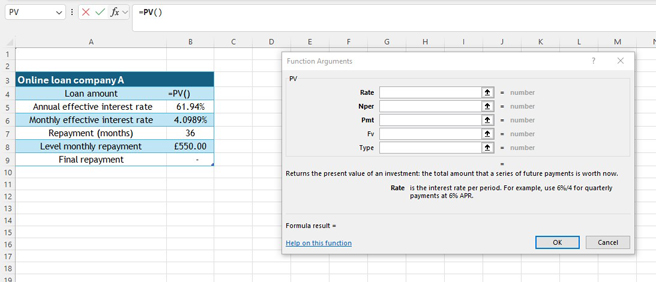

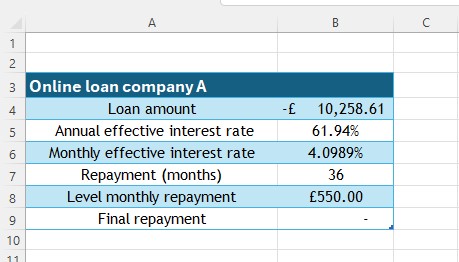

Create a small Excel table with cells for:

- Loan amount

- Annual effective interest rate

- Monthly effective interest rate

- Repayment period (months)

- Level monthly repayment

The monthly effective interest rate can be calculated using:

In the example below, the formula is:

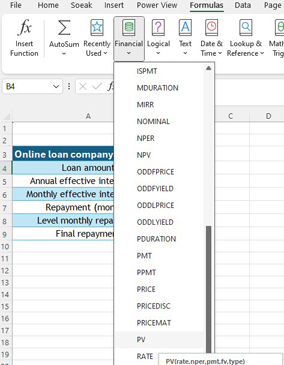

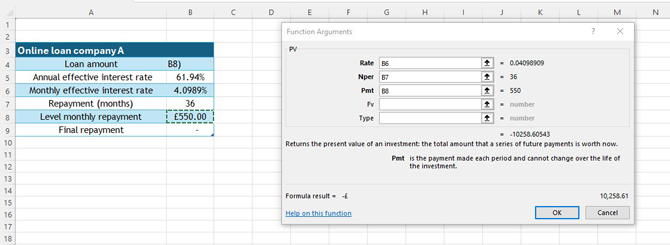

To calculate the loan amount, insert the PV function from the Financial section of Excel’s formula menu:

The following screen appears:

Enter the variables:

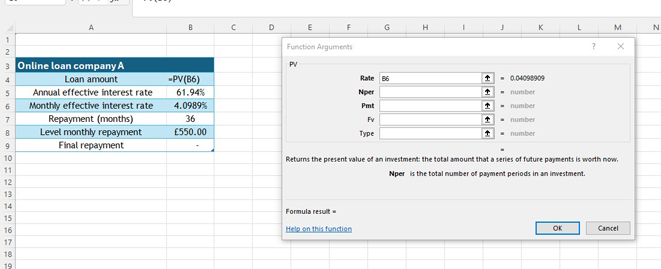

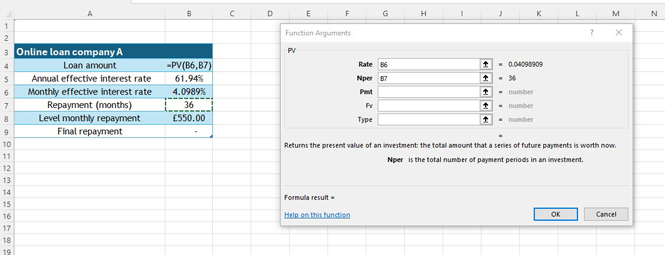

Rate = monthly effective rate (cell B6)

Nper = number of repayments (cell B7)

Pmt = fixed monthly repayment (cell B8)

The loan amount is shown as a negative number (money owed):

4. Solve the mathematical problem

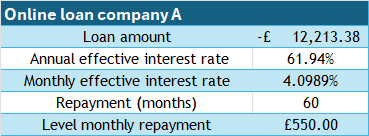

Online loan company A — 61.94% interest

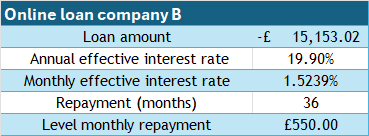

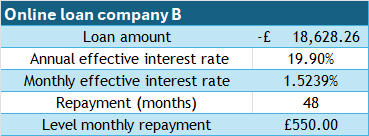

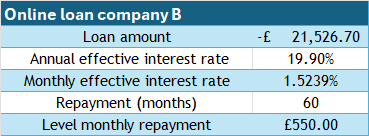

Online loan company B — 19.9% interest

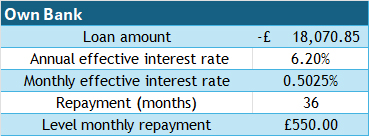

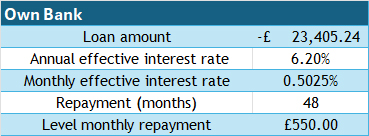

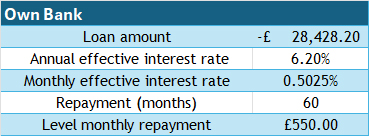

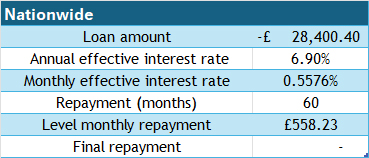

Own Bank — 6.2% interest

5. Interpret the solution

3‑year loan → approx. £18,000 can be borrowed.

4‑year loan → approx. £23,000 can be borrowed.

5‑year loan → approx. £28,000 can be borrowed.

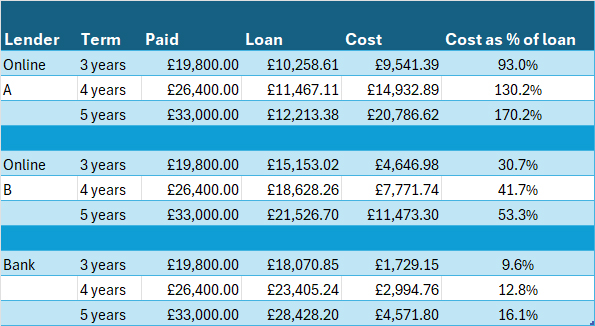

Price range: £18,000 to £28,000

Loan rates depend on credit score. The cost of borrowing varies considerably:

Banks tend to offer much better rates than online finance companies.

6. Compare with reality

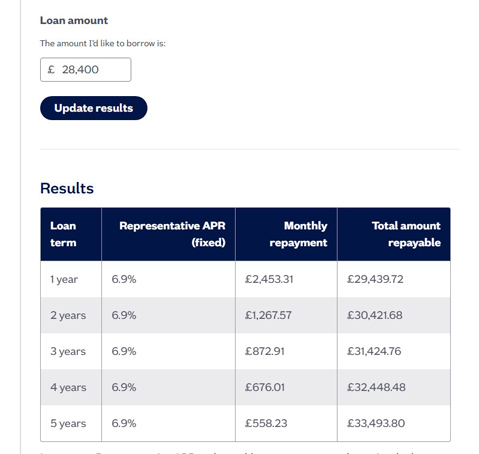

A quick comparison with an online quote:

The model is quite realistic.

Fermi Problems

Named after Nobel Prize winner Enrico Fermi, Fermi problems require reasonable assumptions and estimates to produce approximate answers. Multiple approaches and answers may exist.

How many toilet rolls are required per year for the population of the UK?

Assumption 1: Average person uses 1 roll per week.

Assumption 2: UK population = 66.7 million.

Assumption 3: 85% of population usage.

Estimate:

≈ 2,948,140,000 rolls