Payslips

Payslips come in a variety of designs. They usually show totals, deductions, and personal information, in addition to the actual pay.

Basic Pay = Pay earned during the period without overtime.

Gross Pay = Total income earned during the pay period.

Total Deductions = All money taken off.

Net Pay = Gross pay − Total deductions.

This is what you receive “in hand” or “bottom line”.

Tax Code: This shows how much you may earn before paying tax.

Here, Joe Bloggs can earn £3960 before tax is deducted.

What is Joe Bloggs’ salary?

Joe Bloggs’ annual salary is £25,596.

Paul works a 35 hour week.

He is paid £5.80 per hour.

What is his weekly wage ?

Overtime

Overtime Paid = hourly rate x overtime rate x no. of hours worked

| Overtime Rate | Multiplier | Typical Meaning |

|---|---|---|

| Time and a Quarter | 1.25 × hourly rate | Often used for early overtime or minor extra hours |

| Time and a Half | 1.5 × hourly rate | Very common for weekday or Saturday overtime |

| Double Time | 2 × hourly rate | Common for Sundays or public holidays |

| Double Time and a Half | 2.5 × hourly rate | Used in some industries for bank holidays or emergency call‑outs |

| Triple Time | 3 × hourly rate | Rare; sometimes used for Christmas Day or extreme conditions |

Jack Soap earns £5.78 per hour. He normally works a 37 hour week, but this week

worked an extra 8 hours on Saturday, at time and a half,

and 5 hours on Sunday at double time.

a) How much overtime did he earn ?

b) What is his gross pay for the week ?

a)

b)

Commission

Superannuation

Superannuation contributions are payments made towards a pension.

Pension Contribution = Pensionable Pay × Pension Rate

This is often Gross Pay x Pension Rate , but can be basic pay - depending on the pension scheme.

Fred Ash pays 7% of his gross monthly salary towards his pension.

In January his gross pay was £2145.

Calculate his superannuation.

Joe Bloggs receives a monthly gross pay of £2133.

His superannuation each month is £127.98

What percentage of Joe Bloggs’ monthly salary is paid on superannuation?

Income Tax

Income tax is payable on all taxable income.

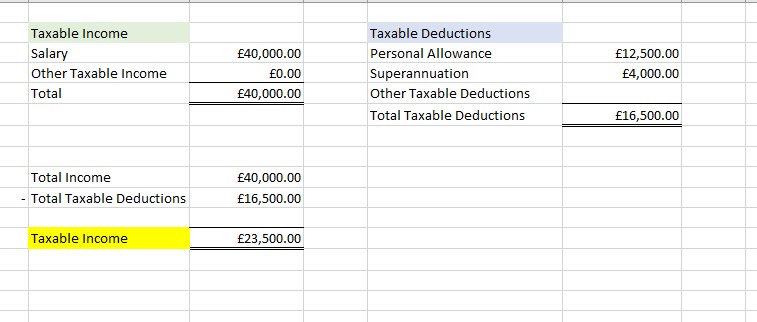

Taxable income = Total income – Personal Allowance – Any other allowances

The rates vary every year, but usually you pay a certain percentage

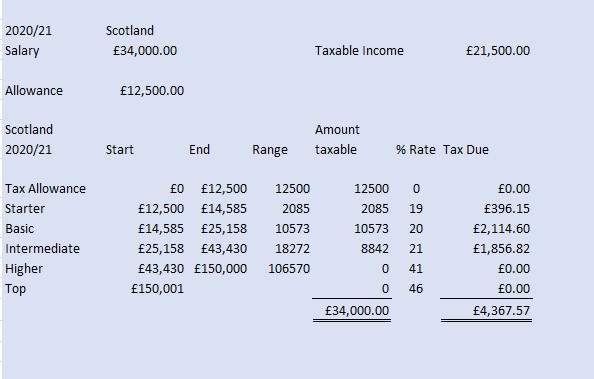

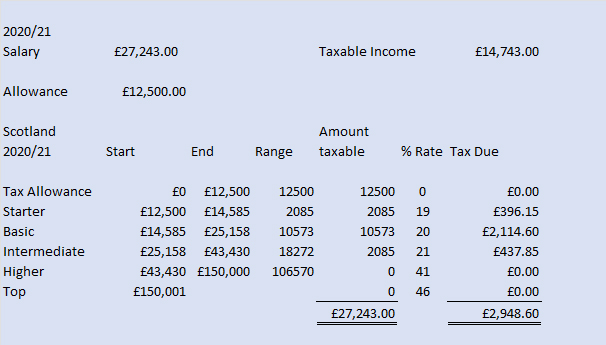

Income Tax: Scotland vs Rest of UK

The following examples compare income tax calculations for Scotland and the rest of the UK during tax year 2020/21.

Source: Tax Bands - Scottish Government

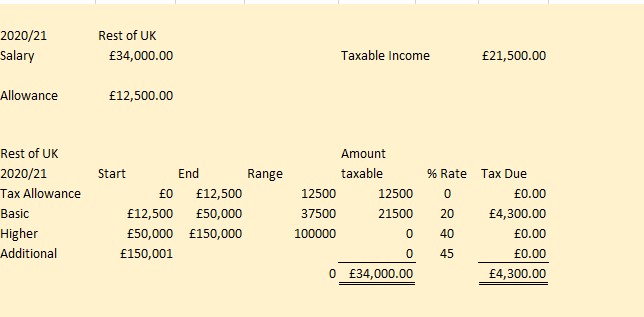

John Doe has a salary of £34,000 and a personal allowance of £12,500. What is the difference in tax paid between Scotland and the rest of the UK?

Scotland

Total Scottish income tax due: £4,367.57

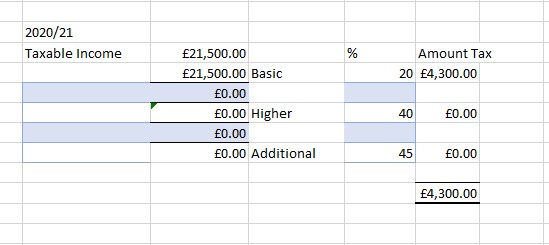

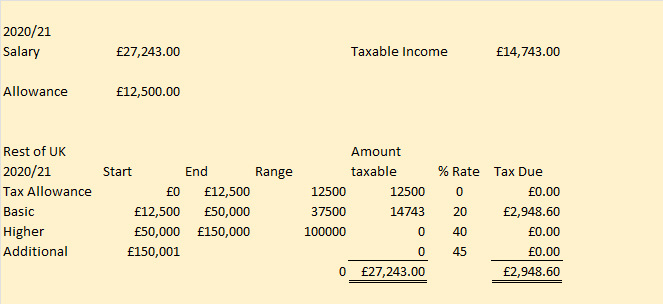

Rest of UK

In the rest of the UK, John pays a flat rate of 20% on all taxable income because £21,500 is below the higher-rate threshold.

Total UK income tax due: £4,300.00

John pays £67.57 more tax in Scotland than in the rest of the UK.

Alternative view

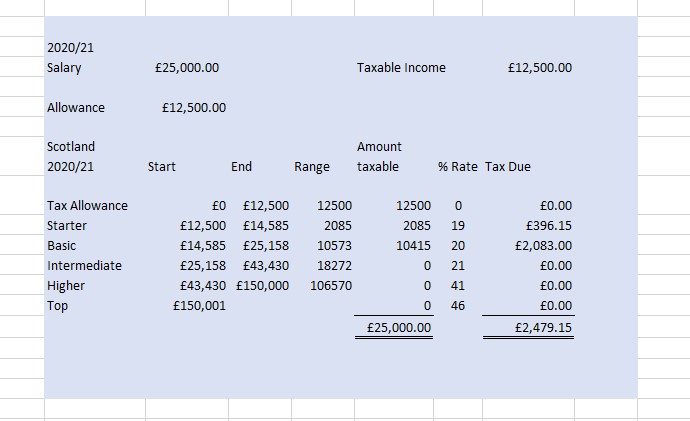

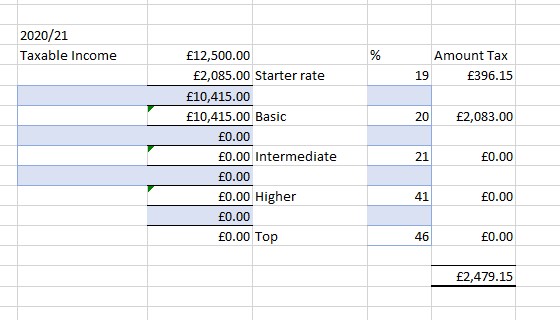

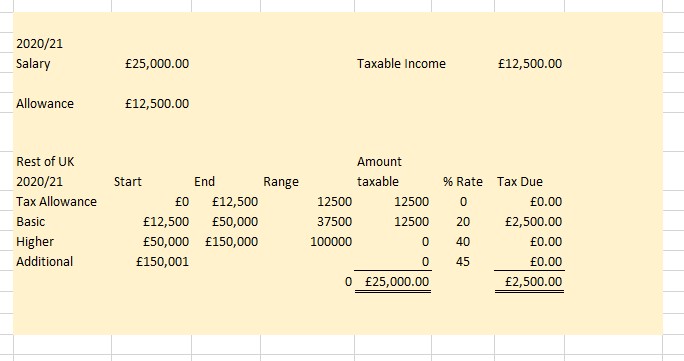

A person earning £25,000 in tax year 2020/21 with a personal allowance of £12,500 would pay £20.85 less in Scotland than in the rest of the UK.

Scotland

Alternative calculation

Rest of UK

Alternative calculation

£2,500 − £2,479.15 = £20.85 less tax in Scotland.

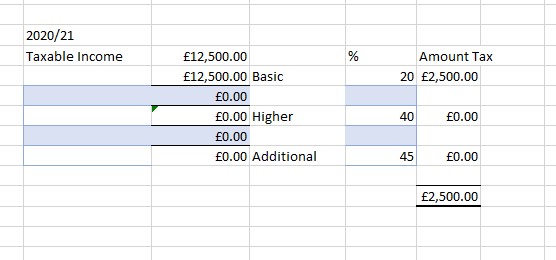

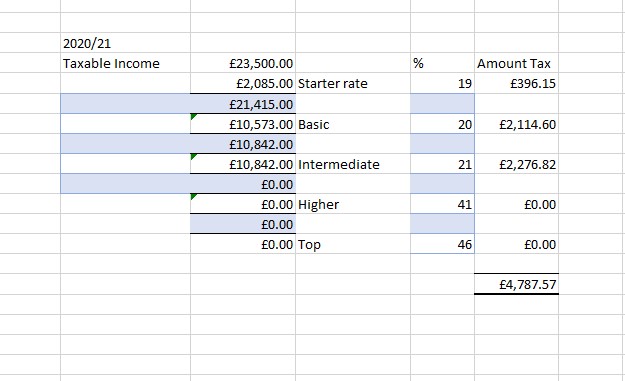

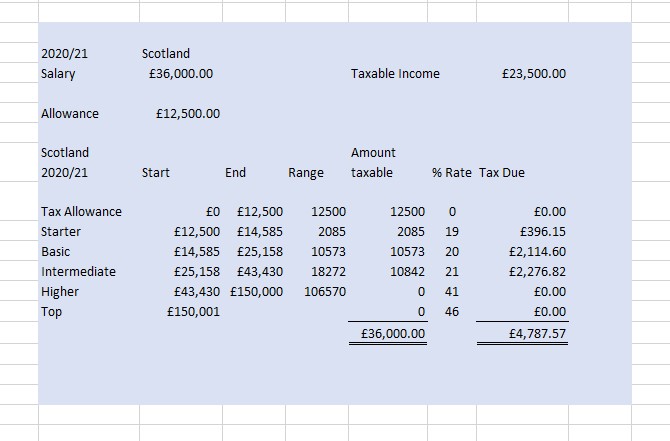

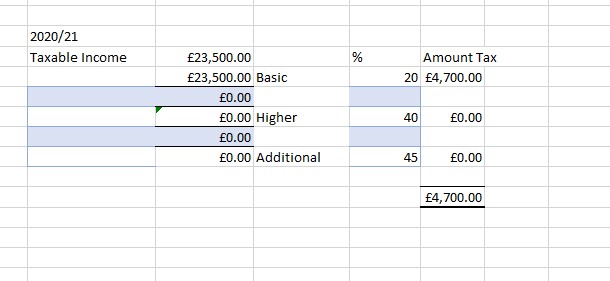

A person earns £40,000 in tax year 2020/21 and pays 10% into a pension (superannuation).

Tax due in Scotland

Or, since pension is tax‑deductible, taxable salary becomes £36,000:

Rest of UK

£4,787.57 − £4,700 = £87.57 more tax in Scotland.

In tax year 2020/21, a salary of £27,243 resulted in equal income tax in Scotland and the rest of the UK.

A salary greater than £27,243 results in more income tax being due in Scotland.

A salary less than £27,243 results in less income tax being due in Scotland.

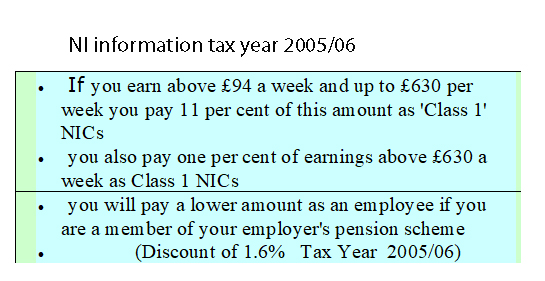

National Insurance

National Insurance Contributions (NICs) are paid in addition to income tax. The earnings threshold is the amount you can earn before NICs are deducted.

For the tax year 2005/06, the earnings threshold was:

- £94 per week

- £408 per month

Using the payslip above:

How much Class 1 National Insurance was Joe Bloggs due to pay per month in 2005/06?

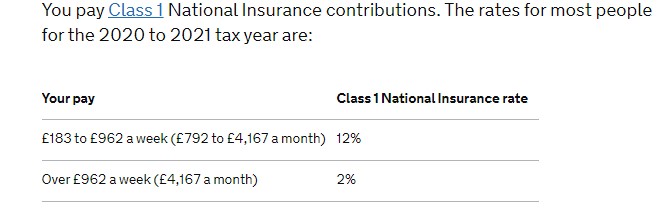

Rates for 2020/21

Using these rates, calculate the Class 1 National Insurance due for John Doe from the earlier example.